|

In our practice, there was a tax evasion scheme revealed, according to which, over several years, the company concealed millions of rubles of unpaid taxes from the state.

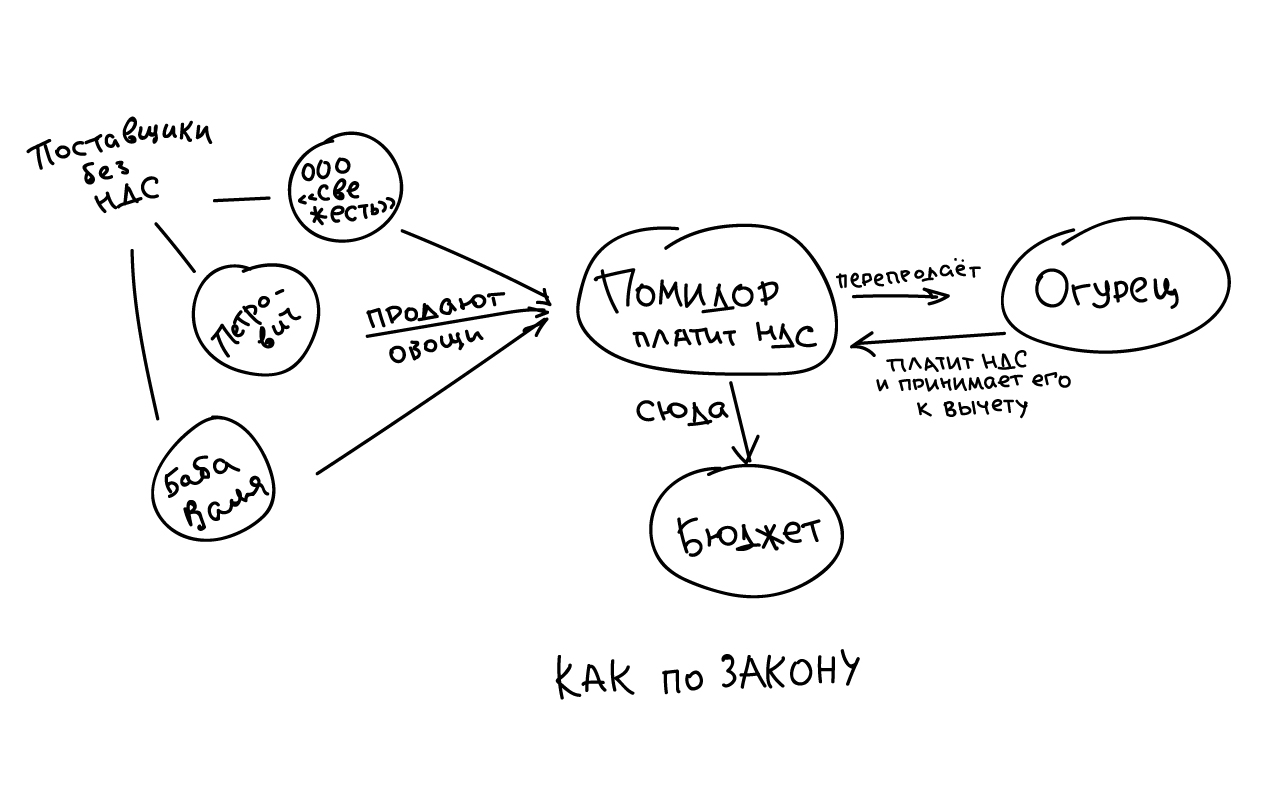

There is some introductory theory

In accordance with Art. 171 of the Tax Code of the Russian Federation, the taxpayer has the right to reduce the total amount of tax calculated in accordance with Art. 166 of the Tax Code of the Russian Federation, by tax deductions prescribed by the Art. 171 of the Tax Code of the Russian Federation. The amounts of tax subject to deductions are the ones applicable to the taxpayer upon the acquisition of goods (works, services) or property rights in the territory of the Russian Federation.

An example in theory

Situation 1. The ‘Cucumber’ company purchases fresh vegetables directly from legal entities and individuals who do not pay VAT. → Contractors do not present VAT to ‘Cucumber’, respectively, it does not have the right to make a tax deduction for VAT on purchased goods.

|

|

That is, if ‘Cucumber’ paid 100 thousand rubles of VAT to ‘Tomato’, then ‘Cucumber’ can deduct these 100 thousand rubles. Accordingly, ‘Tomato’ has an obligation to pay these 100 thousand rubles to the budget. He should not apply the deduction, since he purchased these vegetables from companies that are not VAT payers.

And now the real story

Our ‘Cucumber’ in this story is a taxpayer ‘Agro’ LLC which deducts the amount of VAT presented to it when purchasing goods from ‘Tomato’.

|

|

For example, in the 1st quarter of 2015, ‘Agro’ sold finished production in the amount of 1,300,000 rubles (including VAT at a rate of 18% – 198,000 rubles). These 198 thousand are subject to payment to the budget. If ‘Agro’ directly purchased fresh vegetables from companies that are not VAT payers, then it would not be charged with VAT on these goods, so it would not have the right to make a tax deduction for this amount.

Here, the analogue of ‘Tomato’, ‘OptTorg’ LLC, comes into play and which purchases goods from VAT non-payers. That is, it does not have to pay VAT. Let's say ‘OptTorg’ purchased vegetables in the 1st quarter of 2015 in the amount of 500 thousand rubles.

Watch the hands.

‘OptTorg’ sells ‘Agro’ products. Since ‘OptTorg’ pays VAT, it presents it to ‘Agro’. The amount of VAT at a rate of 18% from vegetables purchased in the amount of 500 thousand rubles, will comprise 90 thousand rubles. ‘Agro’ will pay 590,000 rubles for vegetables, and these 90,000 rubles can be deducted.

When determining the tax base for VAT based on the results of the first quarter, ‘Agro’ deducts 90 thousand rubles from 198 thousand rubles and pays only 108 thousand.

Hmm, it looks like it's legal.

Where is the benefit if ‘Agro’ paid VAT to ‘OptTorg’ and then used its right to a tax deduction?

The application of the tax deduction would be justified if, at the same time, OptTorg paid to the budget the same VAT that it received from ‘Agro’. Those 90 thousand rubles. But ‘OptTorg’ in its books of purchases and books of sales distorts this data in order to ‘align’ the calculated amount of tax with the tax deduction and pay the minimum amount to the budget.

Do you know what is the most interesting? In reality, the amounts were measured not in thousands, but in millions of rubles. Here is the data from VAT tax returns for the first quarter of 2015:

The total calculated tax amount is 9,571,769.36 rubles.

The amount of tax presented to the taxpayer when purchasing goods, deductible – 9,566,387.20 rubles.

The total amount of tax payable to the budget is 5,382.16 rubles.

What is our role in this story?

We acted as experts who helped to prove that taxes indeed were not paid in the amount they should have been. How we managed it – I will tell in the next article.

|